What Is Limited Liability Partnership?

LLP is a popular type of partnership where limited liability Partners enjoy protection of personal assets from debts, liabilities & damages. An LLP is a corporate body and legal entity separate from its partners. It has perpetual succession in every state and is registered under the LLP Act, 2008

An LLP (Limited Liability Partnership) is a corporate business structure that offers its members the benefit of limited liability, just like a company. It allows partners to manage internal affairs based on mutually agreed-upon terms, similar to a partnership firm. Partners have reduced liabilities for any future debts incurred in the course of running the business.

An LLP combines features of both a corporate structure and a partnership firm, making it a hybrid entity that provides the best of both worlds. Partners are required to contribute to the LLP as specified in the LLP Agreement, and their contributions can take various forms, such as tangible or intangible assets, movable or immovable property, money, and cash.

In an LLP, the Company itself is liable for any losses or debts incurred in business operations, which means individual members of the LLP are not personally responsible for such financial obligations.

Documents Required for LLP Registration

Identity and Address Proof

![]() Scanned copy of PAN card or passport (foreign nationals & NRIs)

Scanned copy of PAN card or passport (foreign nationals & NRIs)

![]() Scanned copy of voter ID/passport/driving

Scanned copy of voter ID/passport/driving

![]() Scanned copy of the latest bank statement/telephone or mobile bill/electricity or gas bill

Scanned copy of the latest bank statement/telephone or mobile bill/electricity or gas bill

![]() Scanned passport-sized photograph specimen signature (blank document with signature [directors only)

Scanned passport-sized photograph specimen signature (blank document with signature [directors only)

Registered Office Proof

![]() Scanned copy of the latest bank statement/telephone or mobile bill/electricity or gas bill

Scanned copy of the latest bank statement/telephone or mobile bill/electricity or gas bill

![]() Scanned copy of notarised rental agreement in English

Scanned copy of notarised rental agreement in English

![]() Scanned copy of no-objection certificate from the property owner

Scanned copy of no-objection certificate from the property owner

![]() Scanned copy of sale deed/property deed in English (in case of owned property)

Scanned copy of sale deed/property deed in English (in case of owned property)

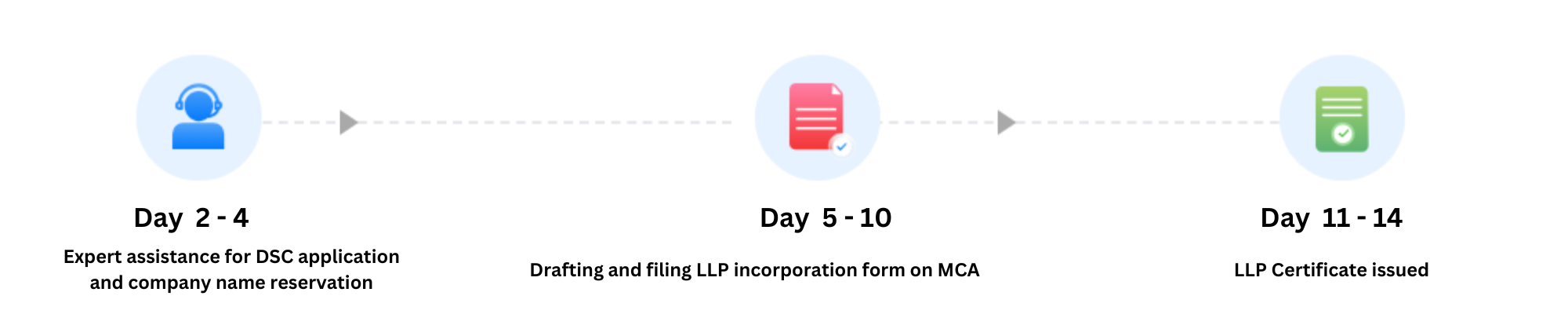

Limited Liability Partnership Registration Process

What we will do

Features of Limited Liability Partnership

LLP is a Body of Corporate

As per Section 3 of the Limited Liability Partnership Act 2008 (LLP Act), an LLP is a corporate body established and registered under the Act. It exists as a distinct legal entity separate from its partners.

Perpetual Succession

Unlike a general partnership firm, a limited liability partnership has the advantage of perpetual succession. This means that even if one or more partners retire, become insolvent, suffer from mental incapacity, or pass away, the LLP can continue its operations. Additionally, the LLP has the capacity to enter into contracts and own property in its own name.

Separate Legal Entity

Similar to corporations or companies, an LLP is recognised as a separate legal entity. It holds full liability for its assets and obligations. Moreover, the individual partners’ liabilities are limited to their contributions to the LLP. As a result, the creditors of the LLP are not considered creditors of the individual partners.

LLP Agreement

The LLP Agreement is a contract agreed upon by all partners, outlining their rights and duties. Partners have the freedom to create the agreement according to their preferences. The Act will govern their mutual rights and duties if they don’t create one.

Artificial Legal Person

For legal purposes, an LLP is considered an artificial legal person. It is created through a legal process and possesses all the rights of an individual. It exists as an intangible, immortal entity but is not fictional since it has real existence.

Common Seal

An LLP may have a common seal if the partners use one (Section 14(c)). However, having a seal is not mandatory. If they choose to use a seal, it must be kept under the custody of a responsible official. The seal can only be affixed by at least two designated partners.

Limited Liability

Under Section 26 of the Act, each partner is an agent of the LLP for its business activities. However, a partner is not an agent of other partners. The liability of each partner is limited to their agreed contribution to the LLP, providing personal liability protection to all partners.

Minimum and Maximum Number of Partners

Every LLP must have a minimum of two partners, and at least two of them must be individuals serving as designated partners. At least one designated partner should always be a resident of India. There is no maximum limit on the number of partners in the LLP.

Business Management and Structure

The partners of the LLP have the authority to manage the business. However, only the designated partners are responsible for ensuring legal compliance.

Business for Profit Only

LLPs are specifically formed to conduct lawful business to earn a profit. They cannot be established for charitable or non-profit purposes.

Investigation

The Central Government holds the power to investigate the affairs of an LLP. They can appoint a competent authority for this purpose.

Mutual Agency

Unlike a partnership firm, in an LLP, actions taken by one partner independently and without authorisation do not make other partners liable. Each partner is considered an agent of the LLP, and the actions of one partner do not bind the others.

Pre-requisites for Incorporating an LLP

- Minimum two partners allowed (Individual or body corporate)

- At least two designated partners are required, with one being an Indian resident

- A digital signature certificate needed

- Mandatory to have an LLP name

- An LLP agreement is essential

- A registered office must be established.

Stages of Incorporation of LLP

Procure Digital Signature Certificate

To file online forms with the MCA, applicants and partners of the LLP need a Digital Signature Certificate (DSC) with a validity of 2 years PAN CARD

Reserve LLP Name

- The new process for reserving a unique name for an LLP involves using the web form ‘RUN-LLP’ (Reserve Unique Name – Limited Liability Partnership)

- This simplified form replaces the old LLP Form 1 and requires basic details and the significance of the desired name

- Applicants can provide up to 2 names in order of preference, ensuring compliance with applicable provisions for name reservation

- If none of the names provided are approved, there is an opportunity to apply for two more names

- The government fees for the RUN form follow the Register Office Fees Rules

- DSC (Digital Signature Certificate) and DIN (Director Identification Number) are not required for filing the RUN form, but having an MCA portal account is mandatory

- Once the name is allotted for the LLP, it is reserved for 90 days from the date of approval.